Energy Costs Spike

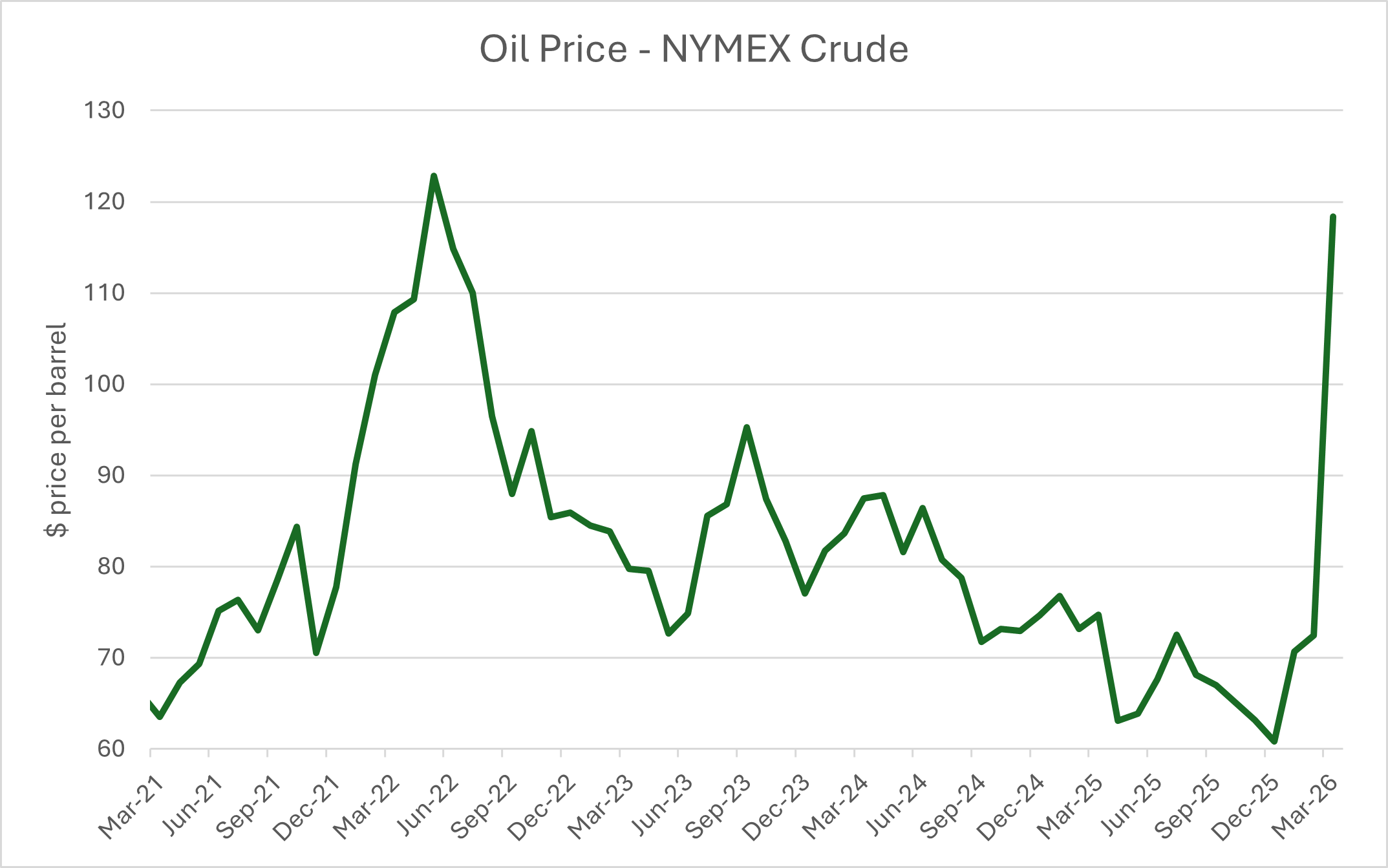

Oil traded in New York advanced from $67 per barrel at the beginning of March to above $100 per barrel to close out the month, as traders assessed the implications of the Iranian conflict. The extreme volatility in oil is a result of military actions effectively choking off a key transportation trade channel, the Strait of Hormuz, that sees supplies of crude oil and natural gas pass through. This is the highest surge in oil since May 2020. Rising tensions is hitting close to home, as the average U.S. gasoline price topped $4 a gallon for the first time since August 2022. The price of gasoline is over $1 more expensive than before the conflict began. Until the conflict can find a longer-term resolution, the price of energy could remain elevated for an extended period.

Federal Reserve on Hold

The March 2026 Federal Open Market Committee (FOMC) kept interest rates unchanged, acknowledging increased uncertainty due to heightened conflicts in the Middle East. The Federal Reserve’s target policy rate is currently at a range of 3.5 – 3.75%. Of note from the meeting, economic forecasts were released with their decision and its inflation outlook for 2026 increased to 2.7% from 2.4%. Elevated inflation stands in conflict with its proposed one 0.25% target rate cut expectation. On top of the stubborn inflation, there has been a notable cooling in the jobs market. These conflicting data points keep future interest rate decisions dependent on either deteriorating further, whether more stimulus is needed to support the economy or higher rates are needed to stem off higher prices.

Value Stocks Top Markets

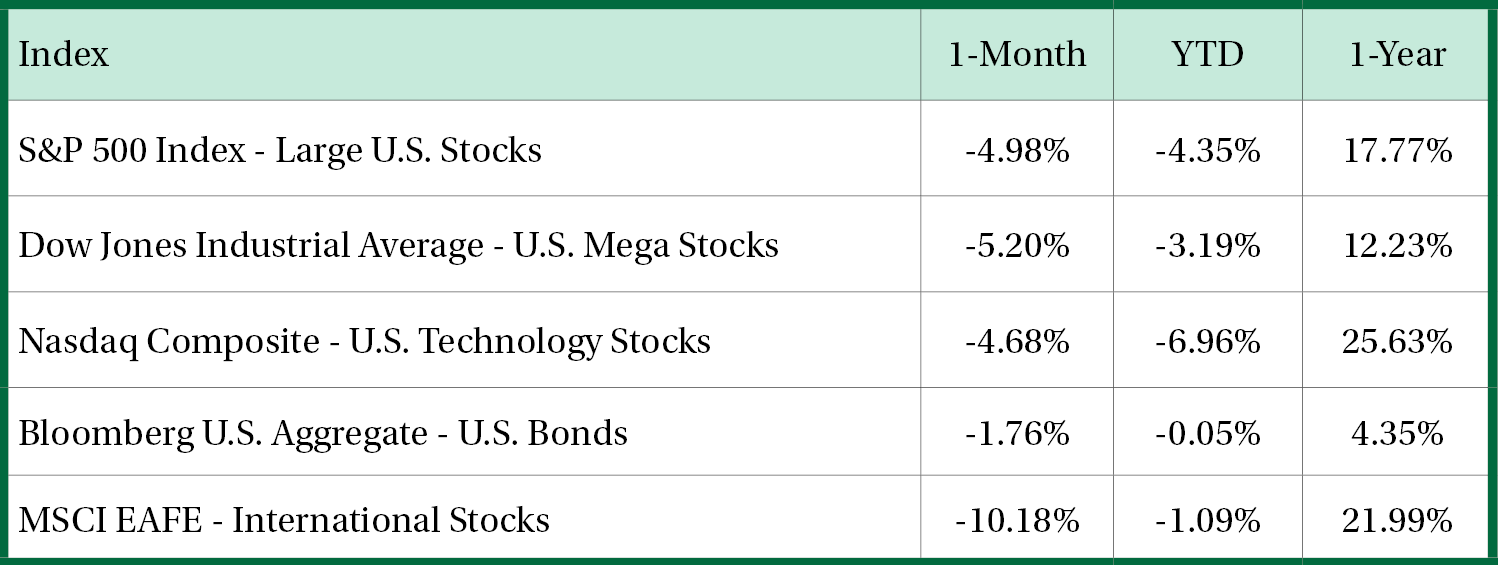

Investor preferences changed in 2026, with the relatively cheaper and predictable earnings of value stocks being in demand. There are a few catalysts for the increased interest: positive earnings trajectory and a higher dividend yield. First, the earnings trajectory has risen over the past couple of quarters, as the technology cohort increased its capital spending that disproportionately supports the value segment’s largest sectors: financials, industrials, materials, utilities, and energy. Despite rising volatility amongst technology stocks, they remain inclined to invest in projects such as data centers and power generation, to name a few. Second, amidst the Iranian conflict, investors have pursued the higher dividend yields of value stocks. Typically, investors prefer immediate return of capital from their investments as opposed to future returns during times of conflict.

U.S. vs. International

The pendulum swung in favor of U.S. markets in March, as international stocks are more susceptible to the conflict given their outsized reliance on resources from the Middle East. Last month the MSCI ACWI ex. U.S., an index represented by international stocks, declined -10.7%, while the S&P 500 index dropped -5%. In conjunction with the economic reliance, the U.S. dollar advanced 2.4%. In times of conflict, investors seek the safety of U.S. assets like the dollar. Advances in the dollar tend to weigh on the performance of international stocks. For international stocks’ outperformance to be regained from last year, two things have to happen: an improved growth outlook or for the dollar to swing lower.

Interest Rates Go Parabolic

The 10-year Treasury yield advanced nearly 0.5% from the beginning of March to the high point of 4.43% on March 27. Most of the increase in the 10-year Treasury yield is attributed to investor expectations of inflation. Longer-term yields are typically influenced by two things: growth and inflation. There hasn’t been any real indication, yet, that growth will be materially impacted, while the impact of inflation has become a greater concern. From a market perspective, investment grade bonds underperformed high yield bonds as the credit risk was impacted less than the higher interest rate risk found in investment grade bonds due to their longer maturities.

Although we believe it to be reliable as of the publication date and have sought to take reasonable care in its preparation, all information provided is FOR INFORMATIONAL PURPOSES ONLY and we make no representations or warranties regarding its accuracy, reliability, or completeness and assume no duty to make any updates in the event of future changes. Past performance may not be indicative of future market results. Any examples used (including specific securities) are generic and meant for illustration purposes only and are not, and should not be interpreted as, offers to buy or sell such securities. To the extent indices are referenced, please note that you are not able to invest directly in an index.

Nicolet Wealth Management is a brand name that refers to Nicolet National Bank and certain of its departments and affiliates that provide investment advisory, trust, retirement plan level services, and insurance services. Investment advisory services offered through Nicolet Advisory Services, LLC (dba Nicolet Wealth Management), a registered investment advisor.

All investments are subject to risks, including possible loss of principal, and are: NOT FDIC INSURED; NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY; AND NEITHER DEPOSITS OR OTHER OBLIGATIONS OF, NOR GUARANTEED BY, Nicolet National Bank or any of its affiliates. Neither Nicolet Advisory Services nor its affiliates offer tax or legal advice. You should consult with your legal and tax professionals before making investment decisions.

Listen & Subscribe to our Podcast

Tune in for the next episode, subscribe or follow us wherever you listen to podcasts.